Adulting 202: How to Buy Health Insurance?

A definitive guide on how, why and where to buy Health Insurance in India — for you and especially your parents.

I turned 27 some months back and with it came a to-do list. One immediate position I took: buy health insurance for yourself, your spouse, and especially your parents — ASAP, and buy a good one.

In India, I know for sure that our parents’ generation ignored or ignore this advice, sometimes due to a lacuna in their experience from the years gone by. State run health systems exist and serve millions every day, and to an extent it used to serve our parent’s generation very well. Even in the case of childbirth or other such large hospitalization-related expenses in the 90s and the early 2000s, state run hospitals and rather affordable mission hospitals or even for-profit private hospitals were considered relatively affordable by those with some modicum of stable income or savings. One hospitalization did not generally push people into a lifetime of poverty like it does in the year of our lord twenty twenty-five.

PSA: If you want to head straight to the crux of this piece, scroll down straight to 'Here is the Fried Rice Recipe' But more on that later. :)

Why is Hyphenated Health-Insurance a Thing in India?

You have ManipalCigna (Cigna is a global Connecticut HQ’d firm), you have NivaBupa (Bupa is a large Australian health insurance firm), Tata AIG (a JV between the century+ old Salt to Software conglomerate, the Tata Group and global insurer we know as AIG and TIL, it stands for American International Group), Bajaj Allianz (Allianz SE you know cause of the Allianz Arena or otherwise), HDFC Ergo (the Ergo Group is from Deutschland) & ICICI Lombard (of the Canadian Fairfax Financial Holdings) and so on…

The insurance sector and consequently the health insurance sector does not allow foreign players. In the early 2010s or late 2009s the poster boy of Indian Economic Liberalization, the then PM, the venerable Dr. Manmohan Singh was on the news all the time due to something called the FDI. As a school-going boy, I knew what it stood for, lest it comes in some General Knowledge Quiz or simply because it was regurgitated in all the forms of news I had at the time.

FDI allowed or allows foreign firms to set up shop for business in India directly (hence the direct investment part) and not go through a million hoops in being treated differently from an Indian firm. This is limited by sector, in Insurance and in some other sectors there exists a limit for this “investment.” No more than 49%, in a firm, which is why these foreign shops set up business with age old Indian firms with brand recognition. Take Bajaj for example, they are a two-wheeler manufacturer that started off assembling Vespa scooters for the Indian market and are now one of the world’s top 10 largest motorcycle manufacturers. Other Indian players known for Vehicle Manufacturing like the Mahindra too have forayed into finance and banking (JV with another Indian familial group Kotak) and of-course lucrative ‘Insurance’. Similarly, the Tatas, a Parsi business family who made their fortune in the Opium trade with the British Empire and China, and then diversified to Trucks, Vehicles and a host of other industries and also relatively recently insurance with AIG.

Just the Fried Rice Recipe?

Regardless, back to business after that short history lesson. I know Uncle Roger just wants the “Fried Rice” Recipe and not the history lesson. I had made the resolution to buy health insurance, yes!

A short why? I had added my parent in the floater employee health policy that my employer provides me for free. How does the floater work? Well say, your employee policy allows for a INR 500K cover in a calendar year. By adding your spouse or your parents, the INR 500K cover remains fixed however the cover can be used for medical expenses towards anyone you have added to the plan. That means claims for your spouse, or parents can be deducted from the INR 500K which usually replenishes in the next renewal cycle or calendar year. You can in most cases choose to increase the cover amount by a few INR 100Ks by paying an increased premium, where you pay just the difference or the amount for the additional “top-up.” In most cases, this whole process of adding a spouse or one or two parents is done without any additional payments by you. However, I have found that in large firms with 100K+ employees where benefits are scarce, the employee ends up having to pay for every additional member they add to the plan, usually besides their spouse or besides their children.

This is where, I decided that the above employee floater plan is not going to cut it and maybe I am better off using this money to get my parent a better plan with more coverage, more spread, less complications, and a wider set of benefits. However, even if you do not have to pay an additional sum to cover your parents in your employee plan, I would still suggest getting health insurance for your parents additionally, outside of this.

Also, there are certain benefits of retaining the company provided health insurance cover for your parents even if you are paying extra? Check the policy details and please verify but in most cases, since employee policies are group policies, meaning a large group of people are covered, singularities like pre-existing conditions such as Diabetes/Hypertension/Asthma etc. don’t lead to denial of health insurance policies, claims or non-acceptance of coverage. Meaning adding your parents to your employee health plan as a floater covers them even if they have the above pre-existing conditions and may be hospitalized due to those conditions. Touchwood, I hope nothing like this happens but the whole point of this is to be prepared.

Why get coverage outside of this? Flimsy health insurance cover from the employers (especially in India) hinge on a low cover amount, lower range of network and cashless hospitals (in cashless hospitals, the bills are claimed to go, the insurer settles them directly without you having to pay first and then reimburse it later from them), no aftercare/before-care coverage, sometimes no special benefits like free health checks, coverage of medicinal support, diagnostic tests both pre and post hospitalization etc. Obviously, this does not apply to you if you are in the 0.01% of the Indian corporate sector which actually gives a damn about their employee well-being and spends a decent sum on these benefits including insurance that covers the employee and their families and covers them well. This is for the rest of us that do not get the same options or those of us working or studying or living in fields outside of this system of coverage.

Here is the Fried Rice Recipe

Step 1: Ascertain the Exact Need

For your parents

- One parent or both? That is one plan or two separate plans.

- Do either have pre-existing conditions? Diabetes (Type I or II), Hypertension, Asthma, Hyperlipidemia, COPD, Obesity (BMI 30+), Coronary Artery Disease.

- If one parent has a pre-existing condition, compare premiums of two separate plans vs one joint plan over 10 years.

- Some plans are made specifically for those with pre-existing conditions or older individuals.

For yourself and your spouse

- One plan where you can add your spouse or children later — newborns are typically auto-added.

- Declare pre-existing conditions clearly, including pre-diabetes.

- Get a full-body health check before buying, after shortlisting a plan.

- If your spouse has a good plan, get added to theirs and invest the INR 20–30K you would otherwise spend into an RD or SIP.

For just yourself (Lone Wolf's welcome)

- If you are active and in a metro, consider: Even, Plum, Loop, Digit, or Navi Health Insurance.

- Even has OPD cover starting from INR 400–900/month — covering pathology tests and small immediate care that racks up bills in the thousands.

- If you are outside Bengaluru, Mumbai, NCR (or Chennai/Hyderabad/Kolkata), go with the traditional options in Step 2.

Step 2: Need Ascertained — Now Choose

- Schedule a call with Ditto Insurance — click Buy Insurance on their site or WhatsApp them at +91-88679-19680. They shortlist plans based on your need and walk you through every detail.

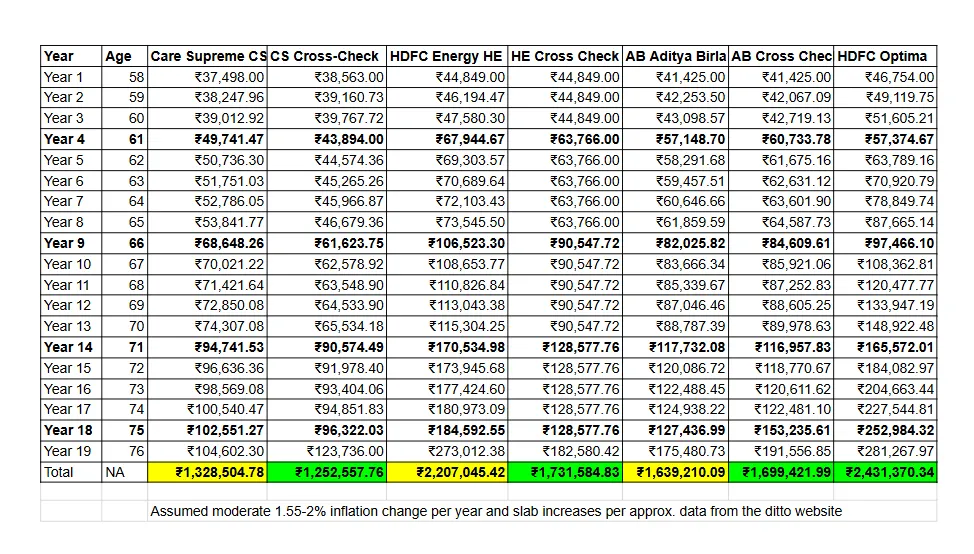

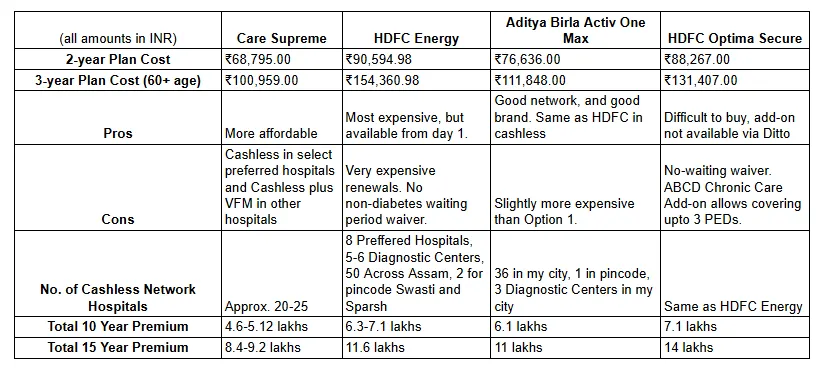

- Once you have a shortlist, model the costs in Excel: plot premiums at your current age, then 5, 10, and 15 years out. Premiums jump when the insured crosses 60 — this matters.

- Ask your Ditto advisor how premiums change across age slabs and cross-verify by toggling age on the insurer's website.

- Check the cashless hospital network in your pincode — Ditto provides the link directly.

- Understand porting: this lets you switch insurers later while retaining cover for pre-existing conditions and waiving the 2–3 year waiting period.

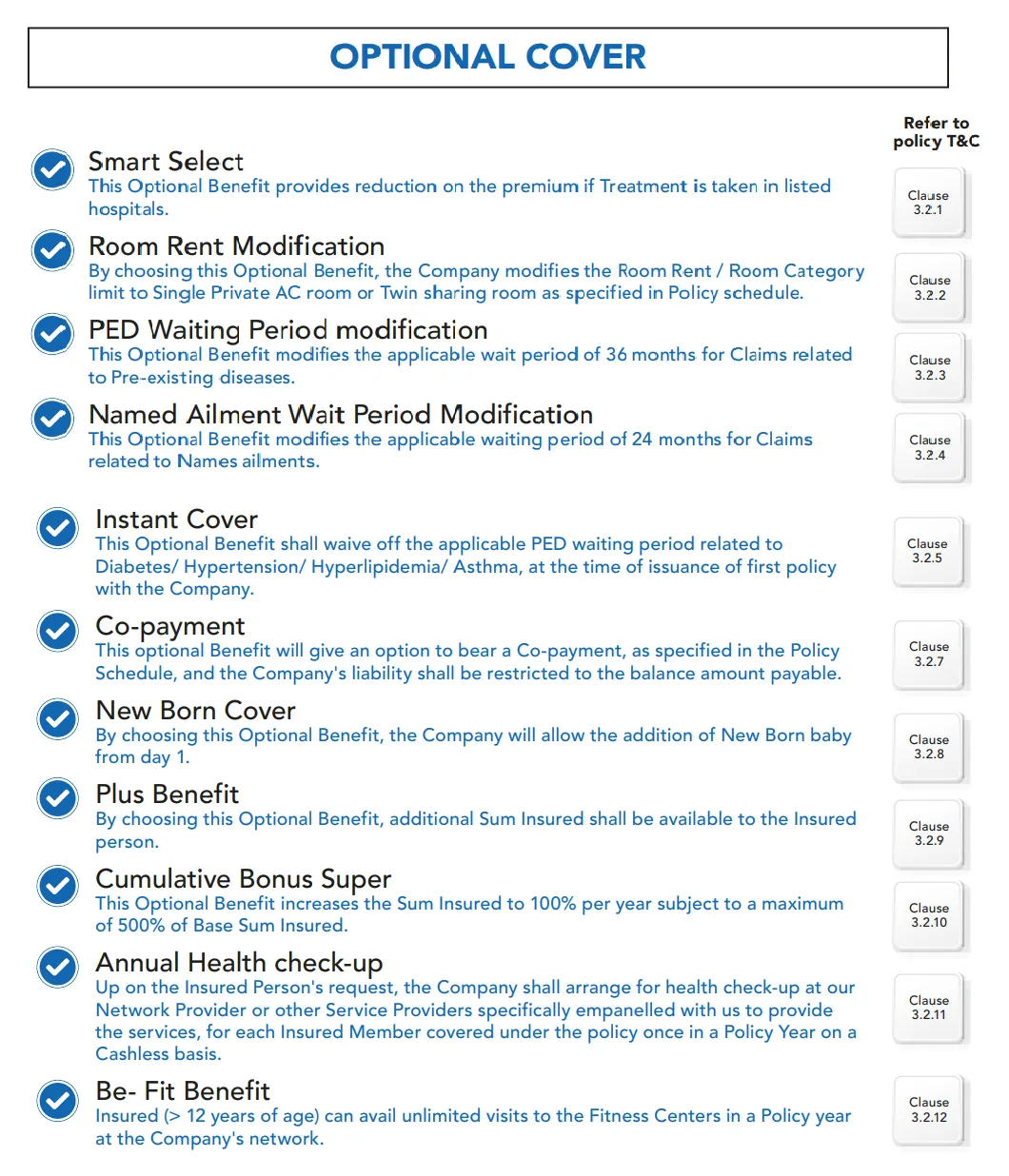

Step 3: Choose Your Add-Ons Wisely

- OPD cover — for outpatient visits and pathology tests outside hospitalization.

- Restoration benefit — cover gets restored if exhausted mid-year.

- Room rent waiver — removes the room rent cap that can otherwise limit your overall claim.

- Critical illness cover and personal accident cover.

- Waiting period waiver for specific illnesses — essential if the insured has pre-existing conditions.

Step 4: Declare Everything

Do not lie to your doctor, your lawyer, your therapist, or your insurer.

- Declare smoking, tobacco use (including Paan), and drinking habits — even if occasional.

- Declare all pre-existing conditions for the insured.

- Heavy smoking may lead to policy rejection — but through Ditto you get a full refund if that happens.

- Be ready for a health test paid by the insurer. Counter-offer if they revise premiums — Ditto does this with you.

- Read the policy documents carefully. Verify all add-ons and declarations are included.

- Share the documents with a sibling or trusted person.

- This is a tax-deductible expense under Section 80D.

What is Not Covered?

- Cosmetic procedures, dental (unless due to accident), vision correction.

- Self-inflicted injuries, war-related conditions.

- Treatment in the first 30 days of the policy (except accidents).

- Always read your specific policy exclusion list carefully.

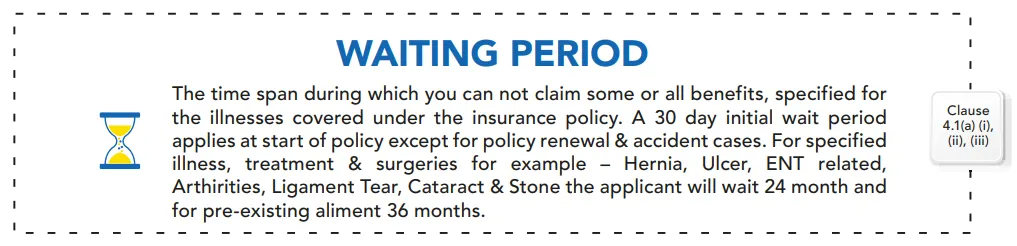

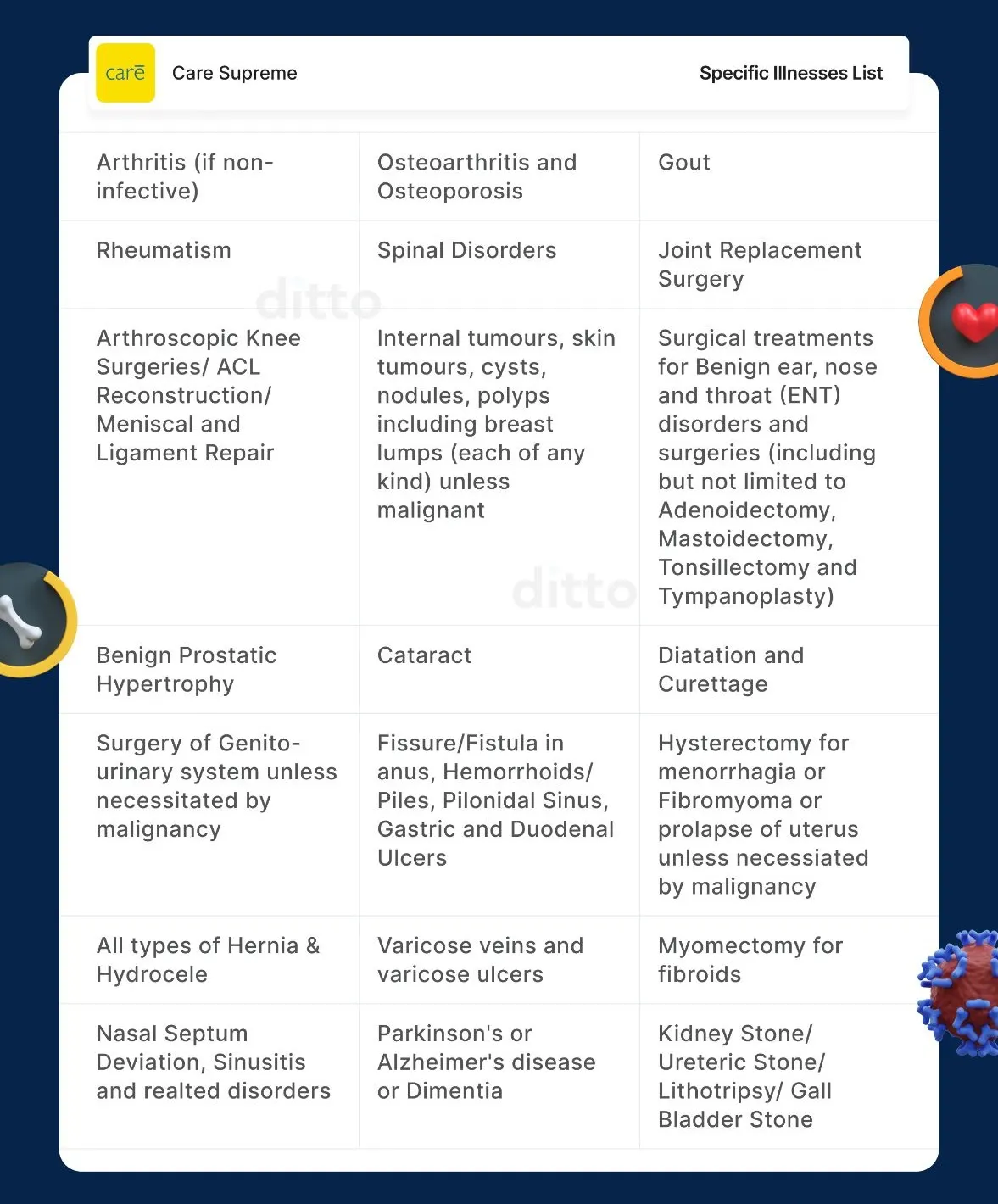

Waiting Period & Specific Illness List

Most plans have a 2–4 year waiting period for pre-existing conditions and specific illnesses. This can often be reduced or waived with a paid add-on. Factor this in when buying for parents who may already have conditions on the list.

Now What?

Chill maadi, cause at best this whole thing (including all the research) will take you 10-15 days and at the very worst, it would take you 2-3 months. 2-3 months is the higher side of the spectrum but is the amount of time I took, as I paused the process in between to deal with some other obligations. It is a shield and it will frankly reduce a bit of the increasing worry you get for your aging parents as you yourself grow older. That said, happy adulting and happy weekend to you!

That said, happy adulting and happy weekend to you!

XoXo - Hrishi

Mandatory Disclaimer: This post describes my personal experience as a listicle. I am not a licensed insurance advisor. Please use Ditto or a qualified advisor for decisions specific to your situation.